.jpg)

For months, you've been juggling work, your own kids, and late-night worry about Mom living alone. You've noticed the little things: the dent on the car she "doesn't remember," the pill organizer that never seems quite right, the almost-fall she laughs off but you can't forget. Somewhere in the back of your mind, you keep telling yourself, "If it gets bad, Medicare will pay for help." After all, that's what it's for... right?

Then the crisis hits. Maybe it's a hospital stay after a fall or a new diagnosis that suddenly makes everything feel urgent. A discharge planner mentions "short-term home health" and" Medicare coverage," and for a moment you can breathe again. But a few weeks later, the nurse and therapist stop coming, the Medicare benefit ends, and you're told that ongoing help with bathing, dressing, meals, or just keeping Mom safe at home is considered "custodial care" — the kind Medicare does not pay for.

You're still working, Mom still needs help every day, and now the question is on you: "How are we going to manage this?"

Myth: "Medicare will cover a caregiver if Mom can't take care of herself."

Reality: Surveys show that well over half of Americans incorrectly believe Medicare will cover long-term care, including help in a nursing home or at home. Families only discover the fine print when they're already in crisis — tired, scared, and trying to make fast decisions about safety, money, and what's fair to everyone.

By the end of this blog, you'll know what Medicare is good at, what it won't pay for, and where home care fits into keeping your parent safe and supported at home.

Medicare is, at its core, health insurance — not "everything my aging parent might ever need" insurance. It's a federal program designed primarily for people 65 and older, with some younger adults qualifying early because of disabilities, End-Stage Renal Disease (ESRD), or ALS.

That distinction matters, because Medicare was built to pay for medical and "skilled" care: hospital stays, rehab, doctor visits, and short-term nursing or therapy — not for the ongoing hands-on help that keeps your parents safe day after day. Long-term assistance with bathing, dressing, meals, or supervision is considered custodial care, and Medicare and most traditional health insurance plans specifically do not cover that when it's the main need.

.jpg)

Think of Medicare Part A as the "hospital and bed-based care" side of Medicare. It's the part that steps in when your parent is admitted as an inpatient, needs rehab in a skilled nursing facility, qualifies for hospice, or needs short-term skilled care at home after a hospital stay. For most people who worked and paid Medicare taxes, Part A feels automatic and "free" because there's no monthly premium — even though there are still deductibles and daily copays.

Under Part A, Medicare helps pay for inpatient hospital stays when your parent is formally admitted: the room, meals, nursing, and the medical supplies and services they need. If they still need daily skilled nursing or intensive rehab after that hospital stay, Part A can then cover a short-term stay in a Medicare-certified skilled nursing facility (SNF) for rehab — not long-term "nursing home" living — provided they had a qualifying inpatient stay and their doctor certifies they need daily skilled care.

Part A may also pay for a limited period of skilled home health care after a qualifying hospital or SNF stay, and it covers hospice care when a doctor certifies that your parent has a terminal illness and a life expectancy of about six months or less.

If Part A is the "hospital bed," Medicare Part B is the everyday medical side — the piece that follows your parent home and into the doctor's office. Part B helps pay for services from doctors and specialists, including office visits, telehealth, outpatient procedures, lab work, X-rays, MRIs, and other imaging.

This is also where most Medicare-covered home health lives. Under Part B, if your parent is homebound and needs intermittent skilled nursing or therapy, Medicare can cover home health visits and a limited amount of home health aide help for things like bathing or getting dressed. That aide support is only covered while the skilled nursing or therapy is also happening and stops when the skilled need ends.

Part B also helps pay for durable medical equipment (DME): walkers, wheelchairs, hospital beds, oxygen equipment, and similar items when a doctor prescribes them. After the Part B deductible, Medicare generally pays 80% of the approved amount.

Original Medicare doesn't really handle the everyday prescriptions your parent picks up at the pharmacy. That's where Part D comes in — optional, separate drug coverage run by private insurance companies. Every Part D plan has its own list of covered medications (formulary),and those drugs are arranged in tiers (lower tiers usually mean lower copays).Starting with the new rules, there's now a hard cap of about $2,100 on annual out-of-pocket drug costs. Once your parent hits that, their plan pays 100% of covered drugs for the rest of the year.

Medicare Advantage (Part C) is the "all-in-one" bundled alternative to Original Medicare through a private insurer. By rule, every Medicare Advantage plan must cover all the medically necessary services that Original Medicare would cover. Most plans also roll in prescription drug coverage (Part D) and layer on extras Original Medicare doesn't cover at all, like routine dental, eye exams and glasses, and hearing tests and hearing aids. Those extras vary a lot by plan and year.

When someone says "we'll bring in home care," they could be talking about two very different things:

Bottom line: Skilled home health sends a nurse to adjust Mom's medications; non-medical home care sends a caregiver to remind her to take them, help her shower safely, make lunch, and keep her company so she's not alone with her worries all afternoon. Together, they can work hand-in-hand — but they are not interchangeable.

.jpg)

When Medicare talks about "home health," it means short-term medical care brought to your parent at home to treat an illness or injury. Under this benefit, Medicare can cover:

Once the skilled need ends, the aide hours end too. Medicare doesn't convert into ongoing daily help.

.jpg)

Medicare home health isn't something you can just "call and start." Four boxes must be checked:

Myth: "Once Medicare starts paying for home health, it will keep going as long as Mom needs help."

Reality: Medicare's home health coverage is temporary and completely tied to the need for skilled care. As soon as your parent no longer meets the medical criteria — or the doctor and agency decide those goals have been met — Medicare home health ends, even if your parent still needs help day to day. What's left (bathing, dressing, meals, supervision, companionship)is considered custodial care, and Medicare expects families, private home care, LTC insurance, or Medicaid to handle that ongoing support.

This is the heart of the misunderstanding: Medicare does not cover long-term, day-in, day-out help with basic personal care when that's the main need. Ongoing assistance with bathing, dressing, toileting, eating, getting in and out of bed, and simple supervision or companionship is considered custodial care, and Medicare specifically excludes it.

Medicare does not pay the room-and-board costs for long-term assisted living, memory care, or a nursing home stay when the primary need is help with daily activities. It also does not cover 24/7 care at home or live-in caregivers.

A lot of what keeps your parent safely at home isn't medical at all: housekeeping, laundry, cooking, grocery shopping, running errands, rides, and simple companionship. Original Medicare treats these as homemaker or custodial services and does not cover them when that's the main need.

Another surprise: Original Medicare does not cover routine dental care (cleanings, fillings, crowns, dentures), routine vision care (yearly eye exams, glasses, contacts), or routine hearing tests and hearing aids — unless tightly tied to a covered medical procedure. Some Medicare Advantage plans add these benefits, but they vary by plan and year.

Medicare is built for hospital and rehab, but most families eventually need day-to-day help at home — and that's exactly where Medicare's support drops off.

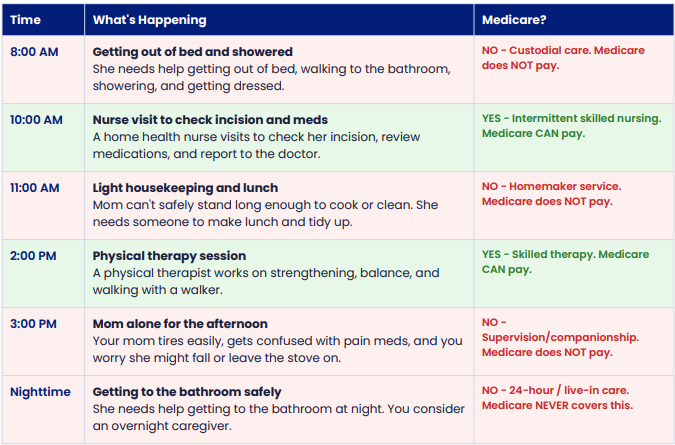

Imagine your mom, six weeks after a fall and hip surgery, now back at home:

The gap between what Medicare will cover and what your parent actually needs day to day is exactly where families start looking at private home care, long-term care insurance, Medicaid, or a mix of family support.

.jpg)

Non-medical home care is the kind of help that keeps your parent safe, clean, and supported on all the days when there isn't a nurse or therapist at the door. It focuses on:

Because this support is considered non-medical and "custodial," Original Medicare does not pay for ongoing non-medical home care. Families usually pay privately (out-of-pocket),through long-term care insurance, sometimes with Medicaid or state programs, or with a mix of resources like VA benefits, life insurance conversions, or specialized state waiver programs.

Myth: "If Mom qualifies for any Medicare home health, she'll get a caregiver as long as she needs one."

Reality: Medicare may cover a limited home health aide while skilled nursing or therapy is active. Once that skilled care ends, the aide stops too. The everyday help — bathing, cooking, companionship — must come from non-medical home care, paid for privately or through other programs.

When you're sorting through all of this, you shouldn't have to do it alone at your kitchen table with a stack of papers and Google tabs. At Castleton Home Care, we sit down with families every week who are asking the same questions you are — what Medicare will cover, where it stops, and how to keep Mom or Dad safe at home without burning out.

We can help you sort through what your parent actually needs, what pieces Medicare and other insurance will handle, and where non-medical home care can realistically make a difference for your family.

We offer a free, no-pressure call or in-home visit where we review your parent's situation together, talk through options, and answer yourquestions — so you can make a clear, confidentplan, whether you decide to use our servicesnow, later, or not at all.

Disclaimer: The information in this article is provided for general educational and informational purposes only and is not intended as, and should not be taken as, medical, nursing, legal, financial, tax, or insurance advice. You should consult with qualified professionals—including, but not limited to, a doctor, attorney, financial planner, or tax advisor—for guidance specific to your situation. Castleton Home Care does not guarantee the accuracy, completeness, or timeliness of the information contained in this article and assumes no liability for any actions taken based on its contents.

.avif)

By clicking "Subscribe Now," you agree to receive periodic emails from Castleton Home Care with updates, news, and special offers. Your information will be processed in accordance with our Privacy Policy. You can unsubscribe at any time.

Subscribe to be updated when new educational videos, local expert interviews, and other written tips and guides for family caregivers are released.

%20(1).jpg)

John Britt, CNA, is the owner and administrator of Castleton Home Care, an independent, non‑franchise in‑home senior care agency serving Alpharetta and North Metro Atlanta. Drawing on formal training as a certified nursing assistant and his experience providing direct hands‑on care in private homes and his local community, he now oversees care quality standards, caregiver recruitment and training, and individualized care planning for older adults who want to age in place safely at home.

John has worked closely with seniors, families, home health nurses, and local senior living communities to coordinate post‑hospital care, support chronic condition management at home, and navigate transitions between home care, assisted living, memory care, and skilled nursing facilities. His practical, evidence‑informed approach emphasizes clear communication, realistic expectations, and care plans that protect safety while preserving dignity, independence, and personal preferences.

As a lifelong Metro Atlanta resident, John is deeply familiar with local healthcare and senior care resources in Alpharetta, Johns Creek, Roswell, Milton, Cumming, and surrounding communities. He regularly shares guidance on aging in place, choosing and managing home care, and comparing local senior care options through educational articles, informative videos, caregiver training, and community outreach so families can make informed, confident decisions.